Eton Pharmaceuticals: A Compelling Speculative Long Leading Into its March 19 Q4 Earnings Report Date

Eton Pharmaceuticals, Inc. (ETON) first came on my radar as a mid-day halt on February 25th. This was for the announcement of FDA approval of DESMODA. The stock initially spiked to nearly $20 but then sold off the rest of the day. As commercialization was set for March 9th and with potential peak sales of $30-$50 million annually, I figured it was worth a flier.

After a couple weeks of more or less flat trading, the stock has bucked the trend of the larger market. That’s highlighted by a 5% rise to $19.02 yesterday. That’s the highest close the stock has had since October. I feel that between the launch and buying leading into the earnings report, this is a good sign.

ETON isn’t your typical biotech small cap. It is achieving revenues from several drugs within its rare disease portfolio. It’s on the cusp of profitability and is operating cash flow positive. So it’s as close to paying dividends as it is to dilution, a rarity for a stock of its ilk. The market has already rewarded the company with about a 5x return from mid-2024 and its valuation multiples are pricing in more growth. So ETON isn’t exactly undervalued.

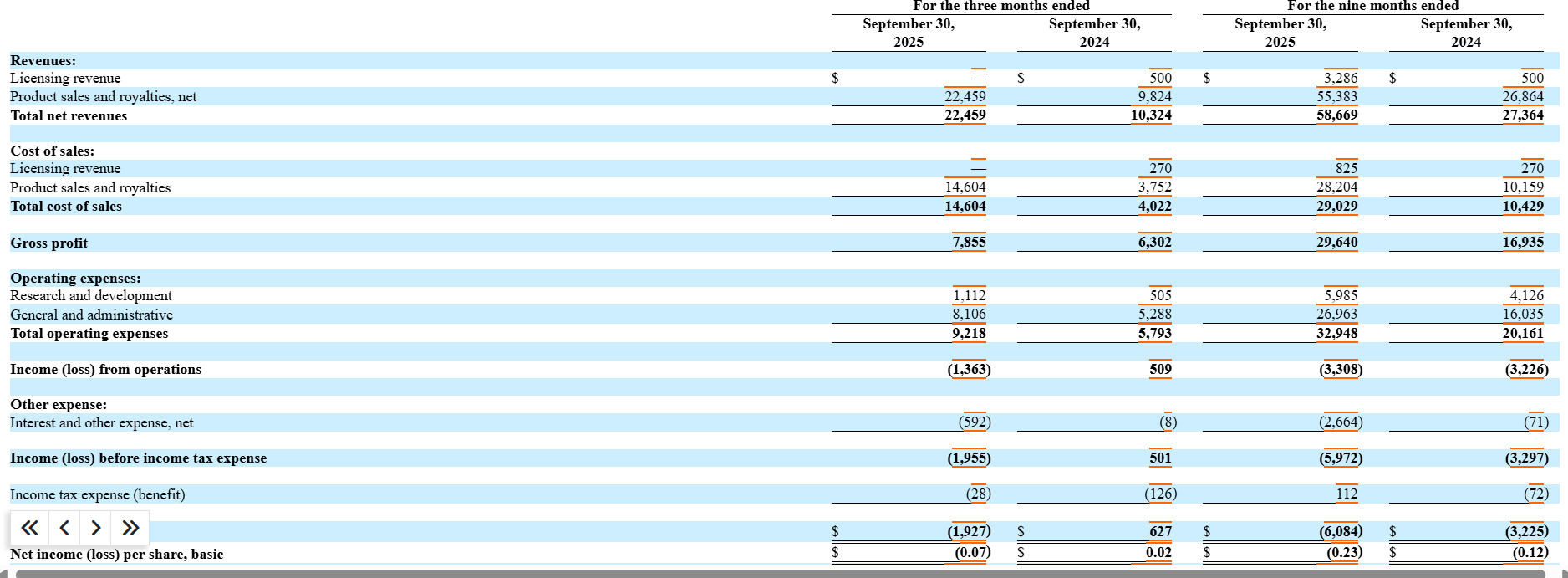

I like it as a speculative momentum play heading into earnings. A snapshot of Q3 earnings shows what we are dealing with:

Analyst estimates on revenue are $79.3 million in 2025 and $105.3 million in 2026. It would need $20.6 million in revenue in Q4 to meet analyst consensus for 2025. ETON has experienced sequential growth in revenue basically since the beginning of time, so it is a decent bet that it can continue to do so going forward:

Management did warn on the Q3 call that while it expects U.S. revenue to sequentially grow, some ex-U.S. revenue is expected to not reoccur in Q4. This may result in revenue being overall flat or slightly down from Q3. The silver lining to this is that U.S. gross margin is over 70% and expected overall gross margin in Q4 is 70%. If this is the case, $20 million in revenue would lead to $14 million in gross margin. $6 million higher than Q3. If opex costs were to remain flat compared to Q3, this would lead to a substantially positive net income, likely in the $4 million range. That would put it at around $0.15 EPS for the quarter, above the consensus of $0.10.

In addition to DESMODA, ETON acquired the rights to commercialize HEMANGEOL. The company plans to roll it out on May 1st, bringing the total numbers of commercialized products in its portfolio to ten. Bringing these two products online during 2026 as well as having organic growth, I’m optimistic that the company will be guiding well above the $105.3 million consensus revenue for 2026.

With a reasonable chance to beat expectations on Q4 revenue, good chance to beat EPS expectations for the quarter and a good chance of guiding 2026 revenue above consensus due to organic growth and two products coming online this year, I like the chances of a positive reaction to ETON’s Q4. Results will be announced after market close on Thursday.

Disclosure: I am long ETON